Have you ever come across the term "call vanna" and wondered what it really means? This intriguing term is often mentioned in the world of finance, particularly in the context of options trading. Whether you're a seasoned trader or a curious novice, understanding the nuances of "call vanna" could significantly enhance your trading strategies. This article aims to demystify "call vanna," providing you with an in-depth look at its application, significance, and impact on the financial markets. So, buckle up as we embark on this enlightening journey into the world of options trading!

In the complex landscape of financial derivatives, "call vanna" plays a crucial role in risk management and pricing strategies. For traders and financial analysts, grasping the concept of "call vanna" is not just beneficial but essential. The term itself might sound arcane, but its implications are far-reaching, affecting how professionals navigate the intricate web of market movements. This guide delves into the mechanics of "call vanna," offering insights into its calculation, practical applications, and potential pitfalls. By the end of this article, you'll have a clearer understanding of how "call vanna" can influence your trading decisions.

Options trading, with its myriad of jargon and mathematical models, can be daunting. Yet, "call vanna" is one of those terms that, once understood, can empower traders to make more informed decisions. This article will not only explain the theoretical underpinnings of "call vanna" but also provide real-world examples to illustrate its impact. Whether you're aiming to sharpen your trading acumen or simply broaden your financial knowledge, this comprehensive guide is designed to equip you with the tools needed to navigate the complexities of "call vanna" effectively.

Table of Contents

- What is Call Vanna?

- Historical Context and Evolution

- Key Concepts and Terminology

- Calculating Call Vanna

- Practical Applications

- Impact on Options Pricing

- Risk Management Strategies

- Call Vanna in Different Markets

- Common Misunderstandings

- Real-World Examples

- Case Study

- Frequently Asked Questions

- Conclusion

What is Call Vanna?

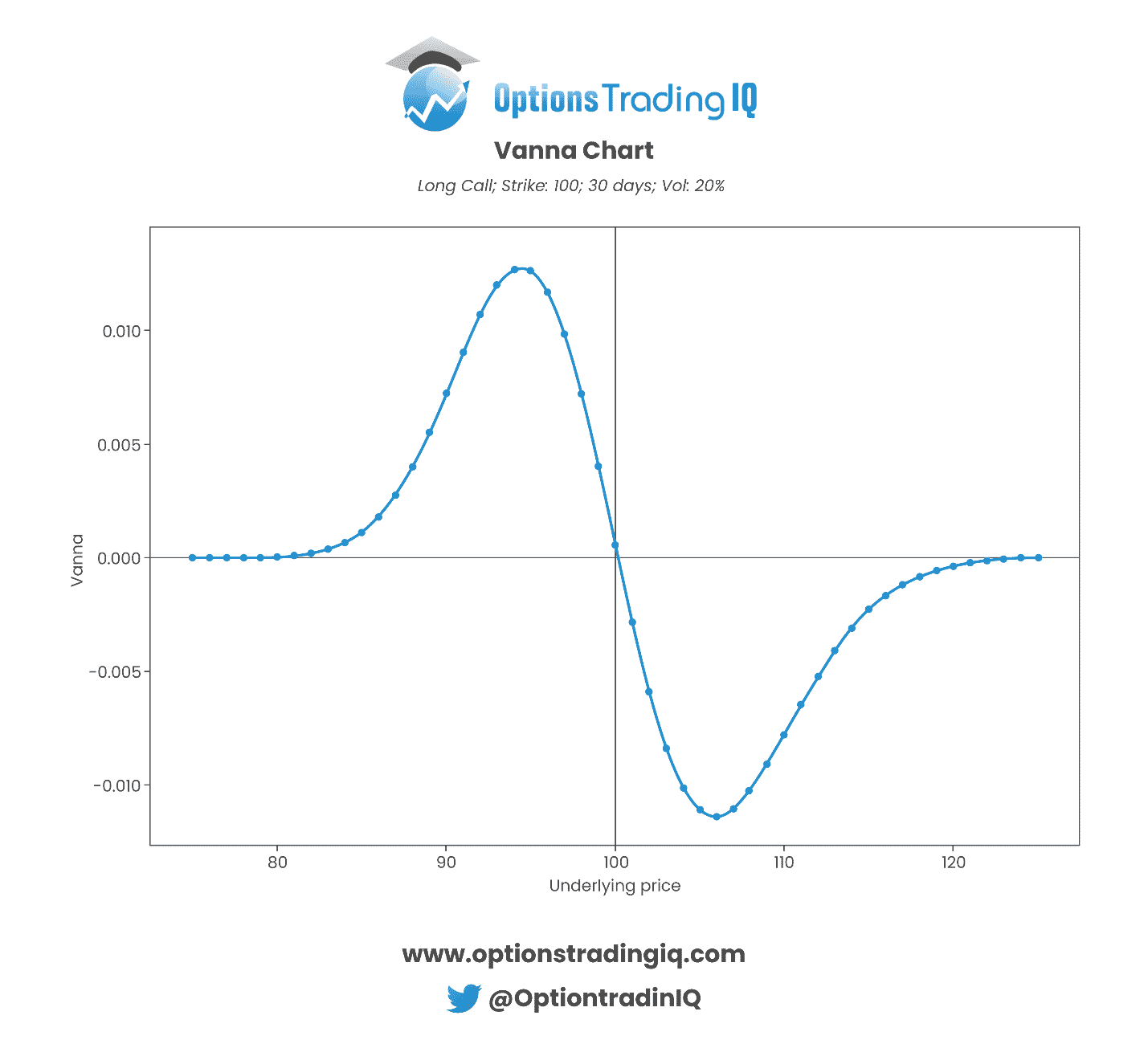

Understanding "call vanna" begins with a dive into the realm of options trading, where it represents a second-order derivative of an option's price. Specifically, "call vanna" measures the sensitivity of an option's delta to changes in the volatility of the underlying asset. In simpler terms, it indicates how the delta of a call option will change when the volatility of the underlying asset increases or decreases. This sensitivity is crucial for traders who rely on precise modeling to predict price movements and hedge their positions effectively.

In the options market, the delta is a fundamental concept representing the rate of change of the option's price relative to movements in the underlying asset. Vanna, in this context, adds another layer of complexity by considering how this delta is influenced by volatility. For instance, if an option has a high vanna, it implies that its delta is significantly affected by changes in volatility, which could alter the option's risk profile and, consequently, its pricing.

While "call vanna" might sound like an esoteric term reserved for the mathematically inclined, its practical implications are far-reaching. Traders use it to refine their strategies, ensuring that their portfolios are aligned with their market expectations. By understanding how vanna interacts with other Greeks like delta, gamma, and vega, traders can better manage the risks associated with their options positions.

Moreover, "call vanna" is not confined to theoretical models but is actively applied in various trading scenarios. Market participants leverage it to adjust their positions in response to changing market conditions, thereby optimizing their risk-reward ratios. Understanding "call vanna" is akin to having an extra tool in the trader's toolkit, allowing for more nuanced decision-making and enhanced market insight.

Historical Context and Evolution

The concept of "call vanna" has evolved alongside the development of the options market itself. Historically, options trading can be traced back to ancient civilizations, where basic derivatives were used for agricultural and commodity trading. However, the modern options market, as we know it today, began to take shape in the 1970s with the establishment of standardized exchanges and the introduction of the Black-Scholes model, a groundbreaking framework for options pricing.

The advent of the Black-Scholes model marked a turning point in the financial industry, providing traders with a mathematical approach to valuing options. This model introduced the concept of "Greeks," including delta, gamma, and vega, which measure various sensitivities of option prices. As traders sought to refine their strategies, the need to understand higher-order sensitivities like vanna emerged, leading to its formalization as a key metric in options trading.

Over the years, the understanding and application of "call vanna" have been shaped by advancements in financial technology and data analytics. With the rise of algorithmic trading and the availability of real-time data, traders can now incorporate vanna into their models with greater accuracy. This evolution has enabled more sophisticated risk management techniques, allowing market participants to navigate volatile environments more effectively.

The historical context of "call vanna" also reflects broader trends in the financial markets, such as globalization and the increasing complexity of financial instruments. As markets have become more interconnected, the ability to manage risk across different asset classes and geographies has become paramount. "Call vanna" serves as a vital tool in this endeavor, helping traders assess the impact of volatility changes on their portfolios and adjust their strategies accordingly.

Key Concepts and Terminology

Before delving deeper into the intricacies of "call vanna," it's essential to familiarize oneself with some key concepts and terminology that underpin options trading. At the core of options trading are the "Greeks," which are mathematical measures used to assess the risk and potential profitability of options positions. These include:

- Delta: Represents the sensitivity of an option's price to changes in the price of the underlying asset. A delta of 0.5, for example, means that if the underlying asset's price increases by $1, the option's price is expected to increase by $0.50.

- Gamma: Measures the rate of change of delta with respect to changes in the underlying asset's price. High gamma values indicate that delta is highly sensitive to price movements.

- Vega: Indicates the sensitivity of an option's price to changes in the volatility of the underlying asset. A high vega suggests that the option's price is more responsive to volatility shifts.

- Vanna: As previously discussed, measures the sensitivity of delta to changes in volatility. It provides insight into how an option's risk profile may change as market conditions fluctuate.

Understanding these concepts is crucial for interpreting "call vanna" and applying it effectively in trading strategies. Each Greek offers a unique perspective on the factors influencing option prices, and together they form a comprehensive framework for risk assessment and decision-making.

In addition to the Greeks, traders often encounter terms like "implied volatility" and "historical volatility." Implied volatility refers to the market's expectation of future volatility, as reflected in option prices. Historical volatility, on the other hand, measures the actual volatility of the underlying asset over a past period. Both metrics play a role in determining the value of vanna and its implications for trading strategies.

By mastering these key concepts and terminology, traders can gain a deeper appreciation of "call vanna" and its significance in the options market. This knowledge serves as a foundation for more advanced analysis and strategy development, enabling traders to optimize their positions and enhance their overall performance.

Calculating Call Vanna

Calculating "call vanna" involves a series of mathematical steps that require a solid understanding of options pricing models and their underlying assumptions. While the exact formula for vanna may vary depending on the specific model used, the general approach involves differentiating the delta of a call option with respect to changes in volatility.

In practice, traders often rely on financial software and tools to compute vanna and other Greeks, given the complexity of the calculations involved. These tools use sophisticated algorithms to process a wide range of inputs, including the option's strike price, time to expiration, current market price of the underlying asset, and implied volatility. By inputting these parameters, traders can quickly obtain vanna values and incorporate them into their risk management strategies.

For those interested in the mathematical underpinnings, the calculation of vanna typically involves partial differentiation of the Black-Scholes formula, a widely used model for options pricing. This process yields a measure of how much the delta of the option will change for a one-unit change in volatility, providing valuable insights into the option's sensitivity to market conditions.

It's important to note that vanna is not a static measure; it can fluctuate based on changes in the underlying asset's price, volatility, and other factors. As such, traders must continually monitor vanna values and adjust their positions accordingly to ensure they remain aligned with their risk tolerance and market outlook.

By understanding how to calculate "call vanna" and interpret its significance, traders can enhance their ability to navigate the complexities of the options market. This knowledge empowers them to make more informed decisions, optimize their strategies, and ultimately achieve greater success in their trading endeavors.

Practical Applications

The practical applications of "call vanna" are manifold, offering traders a powerful tool for managing risk and optimizing their strategies. In real-world trading scenarios, vanna can be used to assess the impact of volatility changes on an option's delta, enabling traders to make more informed decisions about their positions.

One common application of vanna is in the context of volatility trading strategies. Traders often use vanna to gauge the sensitivity of their options positions to changes in implied volatility, which can fluctuate based on market conditions and investor sentiment. By understanding how vanna affects their positions, traders can adjust their strategies to capitalize on volatility trends, potentially enhancing their returns.

Vanna is also valuable for hedging purposes, allowing traders to mitigate the risks associated with adverse market movements. By incorporating vanna into their risk management frameworks, traders can better predict how their options portfolios will respond to changes in volatility, enabling them to implement effective hedging strategies. This proactive approach to risk management helps traders protect their investments and maintain a balanced risk-reward profile.

In addition to these applications, vanna can be used to refine pricing models and improve the accuracy of options valuations. By incorporating vanna into their models, traders can account for the dynamic nature of volatility and its impact on delta, leading to more precise pricing and better decision-making. This enhanced accuracy is particularly valuable in fast-paced markets where timely and informed decisions are critical to success.

Overall, the practical applications of "call vanna" underscore its importance as a key tool in the options trader's arsenal. By leveraging vanna effectively, traders can navigate the complexities of the options market with greater confidence, optimizing their strategies and achieving their financial objectives.

Impact on Options Pricing

The impact of "call vanna" on options pricing is a critical consideration for traders seeking to understand the nuances of options valuation. Vanna, as a measure of the sensitivity of delta to changes in volatility, plays a pivotal role in shaping the pricing dynamics of call options.

At its core, vanna influences how an option's price responds to fluctuations in implied volatility, a key determinant of options pricing. When implied volatility increases, the value of vanna becomes more pronounced, leading to shifts in the option's delta and, consequently, its price. This relationship highlights the interconnectedness of volatility and delta, with vanna serving as the bridge between these two factors.

In markets characterized by high volatility, vanna can have a significant impact on options pricing, as traders actively reassess their positions in response to changing market conditions. For example, during periods of heightened market uncertainty, implied volatility often rises, causing vanna to exert a greater influence on options prices. Traders who understand this dynamic can anticipate and respond to price shifts, positioning themselves to capitalize on market opportunities.

Conversely, in stable market environments with low volatility, the impact of vanna on options pricing may be less pronounced. However, traders must remain vigilant, as market conditions can shift rapidly, necessitating adjustments to their strategies to account for changes in vanna and its effect on pricing.

By understanding the impact of "call vanna" on options pricing, traders can enhance their ability to anticipate market movements and make more informed decisions. This knowledge enables them to optimize their positions, manage risk more effectively, and ultimately achieve their trading objectives with greater precision and confidence.

Risk Management Strategies

Effective risk management is a cornerstone of successful options trading, and "call vanna" plays a crucial role in this process. By understanding how vanna influences delta and options pricing, traders can develop robust risk management strategies that mitigate potential losses and enhance their overall performance.

One key risk management strategy involves using vanna to assess the sensitivity of a portfolio to changes in volatility. By incorporating vanna into their risk models, traders can identify positions that may be vulnerable to volatility shifts and implement hedging strategies to protect against adverse market movements. This proactive approach helps traders maintain a balanced risk-reward profile, ensuring that their portfolios are aligned with their investment objectives and risk tolerance.

Another important aspect of risk management is portfolio diversification, which can be informed by vanna analysis. By understanding how different options positions interact with changes in volatility, traders can diversify their portfolios to reduce exposure to specific risks. This diversification helps mitigate the impact of market fluctuations, providing a buffer against potential losses and enhancing overall portfolio stability.

Traders can also use vanna to refine their position sizing strategies, ensuring that their options positions are appropriately scaled relative to their risk tolerance and market outlook. By considering vanna alongside other Greeks and risk metrics, traders can make more informed decisions about position size, optimizing their risk-reward ratios and maximizing their potential returns.

Ultimately, effective risk management strategies that incorporate "call vanna" enable traders to navigate the complexities of the options market with greater confidence. By leveraging vanna as a key tool in their risk management toolkit, traders can enhance their ability to protect their investments, capitalize on market opportunities, and achieve their financial goals.

Call Vanna in Different Markets

The application and significance of "call vanna" can vary across different markets, reflecting the unique characteristics and dynamics of each trading environment. Traders must adapt their strategies to account for these differences, ensuring that their use of vanna is tailored to the specific market conditions they encounter.

In equity options markets, for example, vanna plays a crucial role in managing the impact of volatility on options positions. Equity markets are often characterized by periods of high volatility, driven by factors such as earnings reports, economic data releases, and geopolitical events. In such environments, vanna can have a pronounced impact on options pricing, influencing how traders adjust their positions and manage risk.

In contrast, fixed-income options markets may exhibit different volatility dynamics, with interest rate changes serving as a primary driver of market movements. In these markets, traders must consider how vanna interacts with other factors, such as interest rate sensitivities, to effectively manage their options positions. This requires a nuanced understanding of the interplay between vanna and other risk metrics, allowing traders to optimize their strategies in response to shifting market conditions.

Commodity options markets also present unique challenges and opportunities for traders using vanna. Commodities are often subject to supply and demand dynamics, seasonal factors, and geopolitical influences, all of which can impact volatility levels. In these markets, vanna can provide valuable insights into how options positions are likely to respond to changes in volatility, enabling traders to make more informed decisions about their strategies and risk management approaches.

By understanding the role of "call vanna" in different markets, traders can tailor their strategies to capitalize on the unique opportunities and challenges presented by each trading environment. This adaptability is key to achieving success in the options market, allowing traders to leverage vanna effectively and enhance their overall performance.

Common Misunderstandings

Despite its importance in options trading, "call vanna" is often misunderstood or overlooked by traders, leading to potential missteps and missed opportunities. Addressing these common misunderstandings is essential for traders seeking to leverage vanna effectively and optimize their strategies.

One common misunderstanding is the belief that vanna is only relevant in high-volatility environments. While it's true that vanna's impact is more pronounced when volatility is elevated, it remains a valuable metric in all market conditions. Traders who dismiss vanna during periods of low volatility may miss out on important insights that could enhance their risk management strategies and decision-making processes.

Another misconception is that vanna is only relevant for advanced traders with deep mathematical knowledge. While a solid understanding of options pricing models is beneficial, traders of all experience levels can benefit from incorporating vanna into their analysis. Financial software and tools can simplify the calculation and interpretation of vanna, making it accessible to a wider range of traders and enabling them to make more informed decisions.

Additionally, some traders may mistakenly believe that vanna is a standalone metric, independent of other Greeks and risk factors. In reality, vanna is interconnected with other risk metrics, such as delta, gamma, and vega, and should be considered as part of a holistic risk management framework. By understanding how vanna interacts with these other factors, traders can gain a more comprehensive view of their options positions and optimize their strategies accordingly.

By addressing these common misunderstandings, traders can unlock the full potential of "call vanna" and enhance their ability to navigate the complexities of the options market. This understanding empowers traders to make more informed decisions, optimize their strategies, and achieve their financial objectives with greater confidence and precision.

Real-World Examples

To illustrate the practical applications and significance of "call vanna," let's explore some real-world examples that demonstrate how traders use vanna to optimize their strategies and manage risk in various market scenarios.

Example 1: In an equity options market characterized by high volatility due to an upcoming earnings report, a trader uses vanna to assess the impact of potential volatility shifts on their options positions. By calculating vanna, the trader identifies positions that are highly sensitive to volatility changes and implements hedging strategies to mitigate potential losses. This proactive approach helps the trader protect their portfolio and capitalize on market opportunities as the earnings report is released and volatility fluctuates.

Example 2: In a fixed-income options market, a trader is concerned about potential interest rate changes and their impact on volatility. By incorporating vanna into their risk management framework, the trader evaluates how their options positions are likely to respond to changes in interest rates and volatility levels. This analysis enables the trader to adjust their positions and optimize their risk-reward profile, ensuring that their portfolio remains aligned with their investment objectives and market outlook.

Example 3: In a commodity options market, a trader is navigating seasonal factors that are expected to impact supply and demand dynamics. By understanding the role of vanna in this context, the trader can anticipate how their options positions will react to changes in volatility driven by these seasonal influences. This knowledge allows the trader to refine their strategies, capitalize on market trends, and enhance their overall performance.

These real-world examples highlight the versatility and importance of "call vanna" as a key tool in the options trader's arsenal. By leveraging vanna effectively, traders can navigate a wide range of market scenarios with greater confidence, optimizing their strategies and achieving their financial goals.

Case Study

To further illustrate the application of "call vanna" in a real-world context, let's examine a case study involving a trader navigating a volatile equity options market during a period of economic uncertainty.

Background: In this case study, a trader is managing a portfolio of call options on a major technology stock. The market is experiencing heightened volatility due to concerns about potential regulatory changes and their impact on the technology sector. The trader is focused on optimizing their risk management strategies to protect their portfolio and capitalize on market opportunities.

Analysis: The trader begins by calculating vanna for each of their call options positions, using financial software to process the necessary inputs and obtain accurate vanna values. This analysis reveals that several positions are highly sensitive to changes in volatility, indicating that their delta is likely to fluctuate significantly as market conditions evolve.

Strategy: Armed with this information, the trader implements a series of risk management strategies to mitigate potential losses and enhance their portfolio's resilience. First, the trader adjusts their position sizes to reduce exposure to high-vanna positions, ensuring that their risk-reward profile remains balanced. Next, the trader uses options spreads to hedge against potential volatility spikes, leveraging vanna to inform their decisions about which spread strategies to employ.

Outcome: As the market continues to experience volatility, the trader's proactive use of vanna enables them to navigate the challenges with confidence. By incorporating vanna into their risk management framework, the trader is able to protect their portfolio from adverse market movements and capitalize on opportunities as they arise. This case study demonstrates the power of "call vanna" as a tool for optimizing strategies and achieving success in the options market.

Frequently Asked Questions

Here are some frequently asked questions about "call vanna" and their answers to help clarify common queries and enhance your understanding of this important concept:

- What is the primary function of call vanna? Call vanna measures the sensitivity of a call option's delta to changes in the volatility of the underlying asset. It provides insights into how delta is likely to fluctuate as market conditions change, helping traders optimize their risk management strategies.

- How is call vanna different from other Greeks? While delta measures the sensitivity of an option's price to changes in the underlying asset's price, and vega measures the sensitivity to changes in volatility, vanna specifically focuses on how delta itself is affected by volatility shifts. It is a second-order derivative that adds depth to risk analysis.

- Can call vanna be used in all market conditions? Yes, call vanna is a valuable metric in all market conditions, providing insights into how options positions are likely to respond to changes in volatility. While its impact is more pronounced in high-volatility environments, vanna remains relevant and useful in all scenarios.

- How do traders calculate call vanna? Traders typically use financial software and tools to calculate call vanna, as the process involves complex mathematical calculations. These tools process inputs such as the option's strike price, time to expiration, and implied volatility to provide accurate vanna values.

- What role does call vanna play in risk management? Call vanna is a key component of effective risk management strategies, enabling traders to assess the sensitivity of their options positions to changes in volatility. By incorporating vanna into their risk models, traders can implement hedging strategies, adjust positions, and optimize their risk-reward profiles.

- Is call vanna relevant for all types of options? Yes, call vanna is relevant for all types of options, including equity, fixed-income, and commodity options. Its significance may vary depending on the specific market conditions and dynamics, but it remains a valuable tool for understanding the impact of volatility on options positions.

Conclusion

In conclusion, "call vanna" is a powerful and versatile tool that plays a critical role in options trading and risk management. By understanding how vanna influences delta and options pricing, traders can optimize their strategies, navigate complex market conditions, and achieve their financial objectives with greater confidence and precision. From its historical evolution to its practical applications and significance across different markets, this comprehensive guide has provided valuable insights into the intricacies of "call vanna." Armed with this knowledge, traders can harness the full potential of vanna to enhance their trading performance and navigate the dynamic landscape of the options market effectively.

For further reading and resources on options trading and risk management, consider exploring external sources such as the Options Industry Council, which offers educational materials and insights into the world of options trading.

You Might Also Like

Discover Unbeatable Pool Cleaner Deals: Your Ultimate Guide To Sparkling PoolsThe Inspiring Journey Of Anisha Isa Kalebic On Instagram

Unveiling The Journey Of Fuller House Ramona: A Star's Rise And Impact

The Healing Wonders Of Port Salt Cave: An In-Depth Exploration

Understanding The Complexities Of Infidelity: A Deep Dive Into "SheWill Cheat"

Article Recommendations